Albert Einstein is often credited with saying “Compound interest is the eighth wonder of the world. He who understands it, earns it; he who doesn’t, pays it”.

In Denmark we all pay it.

It is called lagerbeskatning, a peculiarity of the Danish tax maze that is bad for everyone, and worse for internationals.

But first, a little bit of history.

ACT I

In the beginning of time (1956) there was the Folkepension, in which current workers’ contributions paid for current pensioners. It was good.

In 1964, over fears that public pockets might not be enough to sustain a reasonable income for pensioners, the Arbejdsmarkedets Tillægspension (ATP) was established as a supplementary and compulsory scheme in which workers would save for their own old age. Denmark actually pioneered this idea. It was very good.

The ATP back then had contributions exempt, returns exempt, and payouts taxed.

However, the 70s and 80s inflationary crises meant that pension funds were growing at an explosive rate compared to the economy on people’s doorsteps. Added to unemployment and energy import dependence, this pushed Denmark into recession.

So in 1984 the government introduced the realrenteafgift, a maneuver designed to skim off any pension returns that exceeded inflation + 3,5%. The move also helped finance public debt, which was substantial at the time.

The crisis eventually reverted, but the patch stayed. Before the turn of the century the realrenteafgift evolved to the PAL-Skat (pension yield tax) that exists today, and investment funds/ETFs followed suit shortly after.

And so lagerbeskatning was born.

The difference between realisationsbeskatning and lagerbeskatning is that the former levies tangible money you can use to buy things, and the latter levies the act of saving itself.

Barring peripheral exceptions, it means that you must pay taxes on any gains derived from any broad investments even if you don’t sell them.

Today Denmark is virtually the only country in the world that tributes all long-term mainstream savings products annually. There isn’t a close second. This system is outdated, low-quality, and penalizes international mobility.

ACT II

To begin with, the economic conditions that triggered the realrenteafgift have not repeated since. For 25 years Denmark has enjoyed low unemployment, low public debt, low inflation and sustained economic growth. Denmark’s economy has become remarkably resilient (see 2008 and COVID crises for details).

Now, besides how much we should pay to fund more or less welfare, behind the scenes economists also look at the structural quality of a tax policy. For example:

- Enforceability: A good tax is hard to evade. And indeed, taxes on unrealized gains are hard to evade. Verdict: good!

- Vertical equity: Wealthier people should pay more. How much exactly is the left–right wing quarrel which we won’t resolve today, so verdict: ok.

- Transparency: Compounding is counterintuitive. Most people don’t know how much lagerbeskatning /PAL-Skat costs in the long run. You will learn it in this article. Verdict: not good.

- Neutrality: Normally a tax shouldn’t distort the market. That is, you would make the same decision if the tax on a thing were X% instead of Y%. The current system discourages long-term voluntary investment outside sheltered accounts, aggressively steering savers toward consumption. Verdict: bad.

- Simplicity: Rates on investments follow a hopeless barrage of rules. Exact amounts depend on two realization principles, two income baskets (aktieindkomst / kapitalindkomst), legal structure, at least six (SIX!) types of accounts (frit depot, aktiesparekonto, børneopsparing, ratepension, livrente, aldersopsparing), your municipality (!!), whether an asset is on a Skat “positive” list (!!!), plus special rules for cryptocurrencies, and what not. Verdict: very bad.

- Predictability: When you go to a restaurant, you know that you have to pay moms and how much that is. Predictable. When you invest your savings, you have no idea what your årsopgørelse will be. Thus it becomes harder to know what mortgage to pick, or if you can afford a fancy vacation. You might be forced to sell stock at an inconvenient time just to pay the debt. Verdict: unpredictable and terrible.

- Horizontal equity: People in similar economic situations should have similar obligations and benefits. This is also terrible, and it deserves a longer explanation.

The true engine of the Danish pension system is the overenskomster (collective bargaining agreements) that emerged alongside the ATP. Exact figures vary by sector, but typically for every kroner you put into your pension, your employer puts two more.

Roughly 82% of the working population is covered under one such agreement.

The first bump in the road is that internationals happen to be overrepresented in the remaining 18%.

This is not surprising. Many internationals work for foreign companies without an agreement. Entrepreneurs, startup employees, digital nomads, temporary and part-time workers, many PhD students, workers in the gig economy (all with foreign overrepresentation) are often unprotected too.

This matters because if you aren’t part of an overenskomst and you aren’t a high earner, the deductions for your pension contributions might be less than the social benefits you receive, because the pension payouts reduce your state supplements.

So unless you are saving enough to completely outrun the state’s pensionstillæg, you are effectively punished for working in the “wrong” sector.

Pensions also have other problems for internationals:

- Transferability: The biggest one. If you move abroad, pensions are hard, if not impossible to transfer. EU law permits it, but the Danish system is so idiosyncratic that foreign financial institutions don’t bother with it, leaving you with a frozen account you can’t consolidate.

- Adequacy: They over-index Danish companies, so if you retire abroad you don’t benefit from hedging (that Danish assets protect against Danish cost of living), and might face unfavorable exchange rates.

- Double taxation risk: Denmark has many double taxation treaties, but they lack agreement with Spain (unilaterally cancelled by Denmark because too many Danes were retiring there) and other countries. If you retire in one of them you will likely be taxed twice regardless of your nationality.

- Inheritance complications: Pension funds don’t automatically pass to your estate like other assets, and the process is more problematic for non citizens (Denmark opted out of the EU Succession Regulation and has very few inheritance tax treaties).

This is not a critique of the pension system (OK, it is a bit), but foremost a statement that the existing options aren’t too great for internationals. This wouldn’t be a problem if there were similarly cost-effective alternatives. But…

ACT III

For someone outside the pension system, ETFs are the most accessible long-term savings tool.

Let’s illustrate The But:

- The average person works 42 years in their lifetime

- Average disposable income is ~290.000 kr. / year

- Average household saving rate is 10–13%

- Average nominal market returns are 8–9% globally

- Taxes are 27–42% accrued yearly

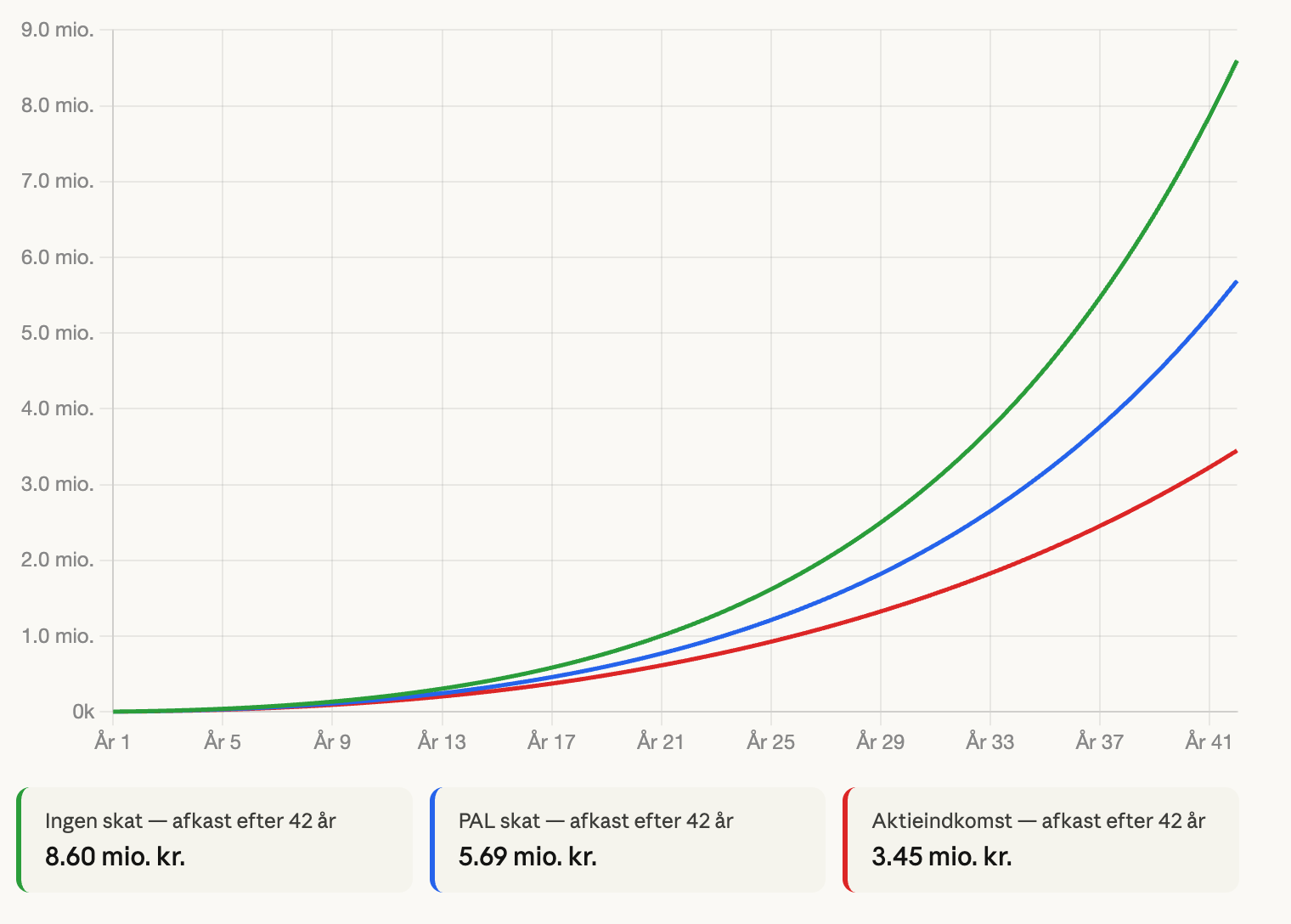

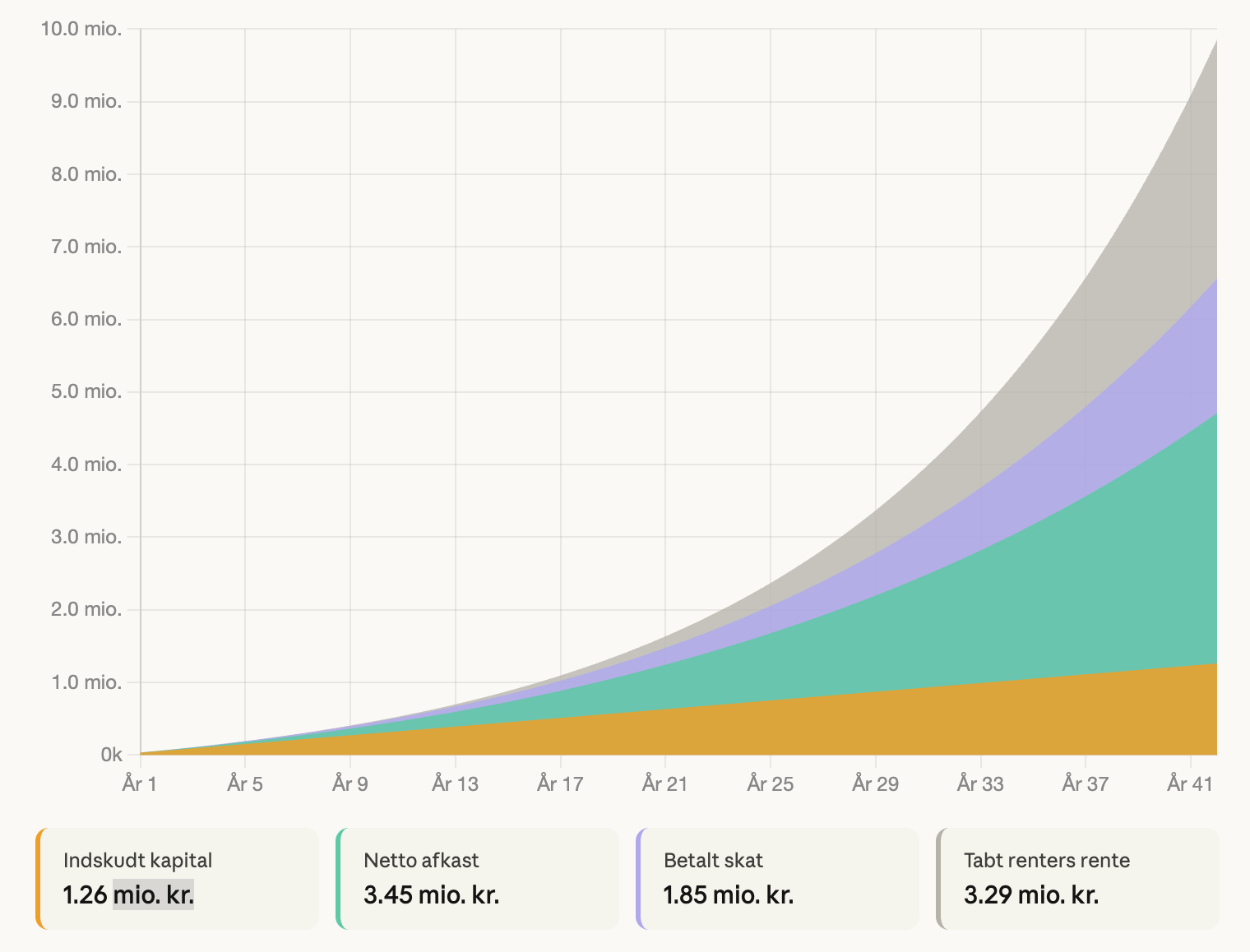

For educational purposes let’s round down and assume that you invest 30.000 kr. annually during 42 years in an ETF with a return of 8%.

- Without taxes, you would have gained 8,6M kr.

- With the current lagerbeskatning you gain 3,45M kr. instead.

- The state takes 1,85M kr.

- The remaining 3,3M are foregone due to not letting interests accrue.

In other words:

- For a modest monthly contribution of 2.500 kr., the total tax drag is ~60%.

- After a lifetime of savings and adjusting for inflation, the spills are not enough to buy a 25 m2 studio in Copenhagen.

- If you were taxed on realized gains at today’s kapitalindkomst rate, both you and the state could be 1,6M better off.

- With increasing retirement ages, this is becoming worse.

That is the power of the compounding effect.

The wealth loss is so bad that the government’s Iværksætterpakke (2024) acknowledges that its own tax system is destructive for Danish companies. Though that acknowledgement doesn’t seem to extend to the individual tax payer.

So how do they justify it?

To my knowledge, two arguments: “equality” and tax symmetry.

ACT IV

Quotation marks because I couldn’t find how exactly, according to the authorities, this tax cocktail is supposed to propel equality.

In fact the toll for investing 2.500 kr. monthly during your lifetime is higher than for inheriting 30.000.000 kr. from Rich Dad in a lump sum. Not a compelling case of egalitarianism.

The off-the-shelf argument is that stock trading is a tool of the rich, so if you tax something that only the rich do, you increase equality. Fair enough… 30 years ago.

Today passive investing is a tool for everybody: 600.000 people have created an aktiesparekonto (ASK) since 2019. Sweden, which doesn’t have lagerbeskatning, has almost 4 million ISK holders. German neighbours are also further ahead.

So the equality argument is bad because it isn’t justified nor credible, and there are better ways to improve it. What about symmetry?

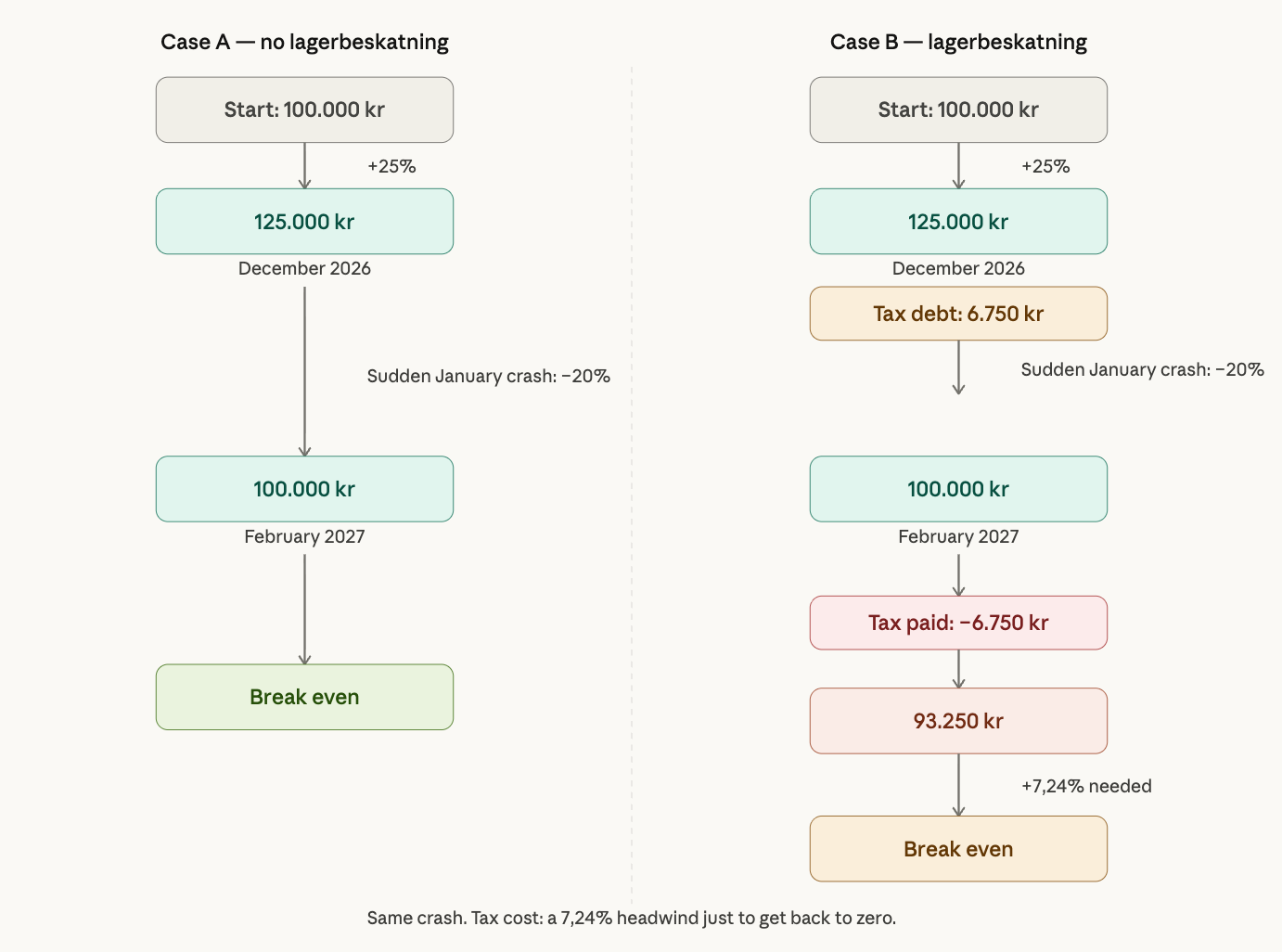

Tax symmetry means that whatever Skat takes from your profit, they give as much on an equivalent loss. This is called a “negative return” and works like this:

- If you have a positive return, you pay with cash.

- If you have a negative return, you don’t get paid with cash (doh). Instead you can offset another gain in the same account. If nothing wins, losses carry forward.

Say for example that you run a standard brokerage account and an ASK during 3 years. Consider this scenario of profit/losses:

| Depot | ASK | Tax | |

|---|---|---|---|

| Year 1 | +10.000 | +10.000 | -4.400 |

| Year 2 | +20.000 | -20.000 | -5.400 |

| Year 3 | +20.000 | -30.000 | -5.400 |

Gains are 10.000 kr. Your bill is 15.200 kr. Alas, a negative outcome on a positive market.

This is not unrealistic.

If you now take out your fundings to buy the dream house that just popped on Boligsiden, you won’t get back the losses nor the tax paid.

If you need to sell because of an unexpected financial setback, same story.

If you get a job opportunity abroad, cancel your accounts, and leave the country? Same story. You might even have to pay an additional exit tax. So much for symmetry!

These are, as far as I know, the “official” arguments. The speculative side of my brain is more inclined to believe that the tax is “just there”, and it is not easy to let go of a predictable revenue stream.

Replacing lagerbeskatning would reduce revenue in the short term, yes. But the current system also destroys long-term wealth that would otherwise recirculate in the Danish economy through consumption, property and inheritance. The “problem” is that governments last 4 years, not long enough to take credit for wealth they didn’t destroy 20 years ago.

So where does this leave us?

ACT V

Between the devil, the deep blue sea and the finansminister.

One of the fundamental freedoms of the EU Single Market (that Denmark is part of) is the right for European citizens to be employed or self-employed under the same conditions as locals in any European country.

Things are harder for non-EU citizens (Denmark being one of the two countries that opted out of the Blue Card Directive), nevertheless since 2008 foreign labor has accounted for 80% of all new jobs created in Denmark. Internationals work more hours and earn less for performing the same work, yet Denmark’s tax policy falls disproportionately on people who move across borders.

So here’s the request:

- Phase out lagerbeskatning, and reform the private pension laws in consideration with internationals and cross-border mobility.

If you can’t access a unionized sector, you should be allowed to save for old age on comparable conditions.

If you leave Denmark and are charged an exit tax, you should get a symmetric exit credit for unrecouped tax losses.

If you can’t transfer your pension, you shouldn’t be subject to a 60% withdrawal fee for taking it with you.

Denmark recruits talent from across Europe and beyond — and that talent moves. The tax system should reflect that reality rather than fight it. Lagerbeskatning doesn’t just hit internationals; it hits anyone whose life doesn’t fit the mold of a single employer, a single country and a single home. That mold is increasingly fictional.

In the greatest physics debate of the XX century, Danish legend Niels Bohr got at least a partial victory over Einstein. When it comes to compound interest though, Einstein was spot on.

great article, thank you Juan!