In this article, I’ll try to untangle some of the confusion around getting a mortgage in Denmark as an international. Personally, I felt a bit lethargic about doing deep research on this topic when I first began my journey of settling down here. I heard stories, even from native Danes, about how complicated and overwhelming the process could be. But over time, as I heard more and more success stories from people who had managed to become homeowners, I started to believe that with the right mindset, a clear plan, and proper preparation, home ownership in Denmark is definitely possible.

That being said, keep in mind that the rules and practicalities can differ depending on whether you’re an EU or non-EU citizen, and the experience will always differ from person to person. While this guide is designed to give you a solid starting point for financing your dream home in one of the world’s most prosperous and happiest countries, I strongly encourage you to research for additional information based on your own situation. Don’t forget there’s a support network out there from financial advisors, family, friends and real estate agents, to buyer advisory services which can make a big difference in your journey.

🏠 Before We Begin: Key Steps to Understand

- Eligibility to own property in Denmark

You must normally either have permanent residency or have lived in Denmark continuously for five years. Permission to purchase is granted through the Department of Civil Affairs under the Danish Ministry of Justice. If you do not meet either of these two criteria, it may still be possible to purchase property depending on your situation. A legal advisor will be able to give further guidance.

👉 Read more here - Define your housing preferences, finding the right property and inspection of the property

Consider whether you want to live in a major city or a surrounding area. Decide on the type of property that fits your lifestyle:

- Owner-occupied homes (Villa og Parcelhus)

- Apartments/Condominiums (Ejerlejlighed)

- Cooperative housing (Andelsboliger)

- Placing a bid and negotiating the price

Once you’ve found the right place, you’ll move on to bidding and negotiating — and hopefully getting your offer accepted. - Final steps after securing the mortgage

This includes reviewing all purchase documents, signing the sale agreement, transferring ownership via the deed (skøde), and purchasing homebuyer’s insurance (ejerskifteforsikring).

For further information about ejerskifteforsikring, read our article.

🏠 How do mortgages work in Denmark?

The Danish mortgage model works differently compared to many other countries. Real estate purchases in Denmark are financed through bonds issued by mortgage credit institutions ‘realkreditinstitutter’. These institutions are separate from banks, and they fund mortgages by issuing bonds with matching characteristics with the specific loan’s terms, such as type, duration, and repayment structure. This model protects the investors in mortgage bonds by making it bankruptcy-remote, meaning that even if the mortgage institution were to go bankrupt, investors will not incur losses. It’s a stable, well-regulated system that benefits both borrowers and investors.

Once the mortgage has been disbursed to the borrower, the bond will be issued at the prevailing market value which in return will determine the rate of the mortgage based on the coupon rate of the bond. In this model, the borrower pays interest, and principal based on the market value of bonds and the margin – “bidragssats”. The margin will be kept by the RealKredit whereas interest and principal will be received by the investor. This model also enables the borrower to prepay and benefit from reduced mortgage prices depending on market conditions.

The general practice is to receive up to 80% of the purchase price as mortgage “RealKredit” and put down 5% of the purchase price as the down payment, which is most common for Danes with a good credit history whereas for internationals it could vary between 5% to sometimes over 30%. This is due to the level of risk the bank would have to accept in lending to internationals . You can also opt into a bank loan to finance the portion above 5%. However, this will be more expensive.

💡 Good to know: Your contributions to the mortgage as interest are tax deductible. This is automatically reported to SKAT.

🏠 Types of mortgages

The main mortgage-related payments include the interest rate, principal repayment tied to the underlying bonds, and the margin charged by the Realkredit institution. This margin covers the costs of loan administration, a risk premium in case of default, the return on capital used to fund the loans, and the accumulation of capital buffers. I’ve included a brief note on these margins so you can factor them in when assessing the total cost of different mortgage types.

All mortgage rates and repayment prices in Denmark are determined by the type of mortgage and the prevailing market price of the underlying bonds or short-term interest rates. This means that, as a borrower, you generally cannot negotiate the interest rate itself.

Read the below types of mortgages in detail for your understanding:

- Fixed-rate Mortgages

These mortgages specify the interest rate for the next 10–30 years depending on your mortgage period, and during this entire period, the rate will be fixed. The interest rate in the market could vary depending on the bonds available in the financial markets.

However, also note that the mortgage loan will be taken at a value less than 100. It’s normal, as a rational borrower, to aim for a price that is as close to 100 as possible to avoid the exchange loss (the mortgage value and the proceeds you receive).

You also have the opportunity to prepay the mortgage prior to the settlement dates: 31 January, 30 April, 31 July, and 31 October. This, however, will result in a differential penalty (not more than 6 months of interest; this is tax-deductible).

The prepayment for this mortgage can take two different forms:

✔ Prepayment at the par value (100)

✔ Prepayment at the market value (when the interest rates are lower in the market, the underlying bond is bought at a value below par – also known as refinancing)

- Variable-rate Mortgages (F1,F3,F5,F10)

Also known as adjustable-rate mortgages, these are long-term bonds funded through short-term bullet bonds. The “F” in F1, F3, F5 indicates how often the interest rate resets- every 1, 3, or 5 years respectively, based on the interest rate of a newly issued underlying bond.

These mortgages are taken at par value (100), therefore they are a good alternative to avoid the exchange loss and ensure the total principal value is lower. In addition, the interest rates under this may be lower than fixed-interest loans. However, as the borrower you must consider the interest rate risk arising from future interest rate adjustments.

If the underlying bond for variable-rate mortgages is a callable bond, prepayment could be tricky. If you pay before the deadline, it will be at the market value, which could make the mortgage more expensive than initially predicted.

- Floating-rate Mortgages (with or without interest rate cap)

When you take on a long-term mortgage that is financed by short-dated floating-rate bonds, the interest rates may vary every 3–6 months under this mortgage type. That’s one of the main differences compared to variable mortgages. The rate is also determined by referencing market rates, including the Copenhagen Interbank Offered Rate (CIBOR) or the Copenhagen Interbank Tomorrow/Next Average (CITA), plus a premium.

Floating-rate mortgages can also be taken with an interest rate cap to reduce the risk of significantly increased interest rates.

Additional Information for You About Bank Loans and Margins

Margins / Bidragssats – This is another important cost variable you should compare between financial institutions. The rate will also take into account your LTV (Loan-to-Value ratio) and the type of mortgage (e.g., installment-based) when determining the final rate. You can get a rough estimate using this link: https://www.mybanker.dk/sammenlign/bolig/bidragssatser/

Home Loans – If you cannot finance the portion that’s not covered by the mortgage, the bank may offer you an additional bank loan to cover the amount above the mandatory 5% of the total mortgage value. The interest rate for this can be negotiated directly with the bank, and no margin (bidragssats) will apply to these loans.

🏠 Now, organize your finances and have a very clear understanding of where you stand.

- Financial Position – Consolidate all your financial assets and liabilities including investments, loans, leases etc and have your net financial position figured out.

- Personal/Household Budget – Prepare a detailed monthly budget specifying your income streams, financial commitments, and your savings savings. Ask yourself whether you can understand your cash flow position at the end of every month. Extend this if you are a family to understand the household income and your position at the end of every month.

- Down Payment – Have a rough idea of how much you are willing to put down as the down payment. Although the bank’s required amount may impact this decision, it’s important to know the state you will be comfortable in, depending on your aspirations and willingness to take a financial risk.

- Debt-Income Ratio – Calculate your debt factor or the leverage in terms of your financial position as well as your debt-income ratio. This is extremely important in the process.

- Supporting Documents – Make sure you have all the documentation ready about your payslips, financial assets and liabilities including overseas, pension, SKAT reports, and fixed payments.

🏠 Applying for a Mortgage

Almost every bank has a section dedicated to mortgages, and they will require you to open a personal bank account with them as part of the process. You can complete the contact or book-a-meeting section on the bank’s website of your choice and schedule an in-person conversation. You can also do this through your real estate agent, which a few of my friends have done.

From my own experience, they will screen your entire background, so it’s a good idea to have all your information ready. This helps guide the conversation and allows for more detailed discussions. Ultimately, it’s about how truthfully and confidently you can present yourself as a strong candidate for the mortgage.

Be ready with your;

✔ Personal profile, immigration history and visa status

✔ Education and career background

✔ Information on your finances including assets overseas (ideal to be detailed but not necessarily required for the initial discussion)

Credit Assessment

If you are applying for a mortgage and a bank loan, it’s important that you also are aware of how you will be assessed. Primarily, you will be assessed based on;

✔ Your income and savings

✔ Your net worth

✔ Your capacity to meet any potential increase in interest rates

✔ Loans – Loan-to-value limits, the value of a loan relative to the value of a property

The following are some of the key elements banks use when assessing your creditworthiness, although they may also consider other individual factors.

Gældsfaktor – Your DTI (Debt-to-Income Ratio)

This is a measure of how much debt you carry relative to your income and helps determine the maximum property price you can afford.

Banks place significant importance on this factor and typically ensure that you don’t borrow more than 3.5 times your annual disposable income, even if your monthly budget could handle the repayments. However, this can be discussed with your bank. Your financial advisor may also take into account your overall profile, such as your career potential, job security, and net worth, when assessing your gældsfaktor.

It’s commonly known that if you’re a young, high-potential borrower, the bank may accept up to 4 times your disposable income. For middle-aged applicants, this typically ranges between 2–3 times, depending on the case.

Rådighedsbeløb – Disposable Income After Fixed Costs

Banks also assess your ability to cover essential living expenses after paying your fixed monthly commitments, including your mortgage. You should have enough left over to support yourself (and your family, if applicable) while still being able to meet your interest obligations.

The expected minimum rådighedsbeløb is usually:

✔ 4,000–5,000 DKK per adult

✔ +2,500 DKK per child

This ensures that you’re not only able to afford the mortgage today, but that you can also continue to afford it in the future — even if interest rates rise or your financial situation changes.

Loan to Value Limit – This value is limited to 80%.

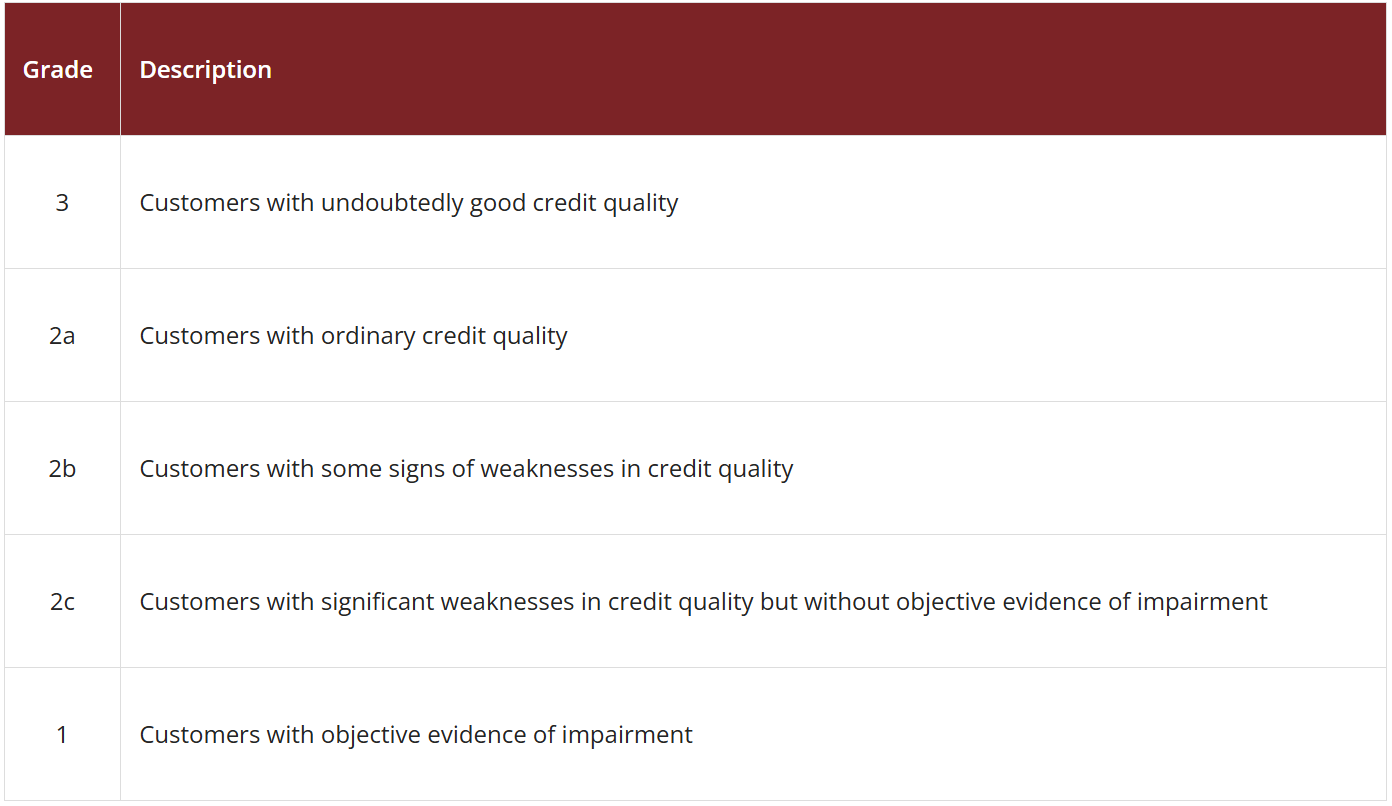

The infographic below illustrates how banks will characterize a borrower’s lending quality.

💡 Additional Note: The Finanstilsynet has given separate detailed guidelines for the financial institutions associated with mortgages and loans granted in high growth areas. The municipalities covered are thus Copenhagen, Frederiksberg, Dragør, Tårnby, Albertslund, Ballerup, Brøndby, Gentofte, Gladsaxe, Glostrup, Herlev, Hvidovre, Høje-Taastrup, Ishøj, Lyngby-Taarbæk, Rødovre, Vallensbæk and Aarhus.

🏠 Mortgage Institutions

Finally, what are the credit institutions who will provide you with a mortgage and the banks who will finance your bank loan? Note that your financial advisor from the bank will be the intermediary between you and the credit institution.

Be mindful that my list is not exhaustive.

💡 Good to know: you should compare the fees, charges and interest among many other facilities when choosing the bank to proceed with your mortgage application.

| Banks | Mortgage credit institutions |

| Danske Bank | Realkredit Danmark |

| Nordea | Totalkredit |

| Jyske Bank | Nykredit Realkredit |

| Sydbank | Nordea Kredit |

| Lån & Spar | Jyske Realkredit |

Also, remember that these financial institutions are bound by the principle of “No Termination Without Cause”, which means that — except in the case of default — mortgages cannot be terminated or renegotiated annually. This provides long-term security and predictability for borrowers.

I hope this has given you a solid overview of how mortgages and loans work in Denmark. I understand it can be quite confusing, especially when compared to other European countries , and it’s certainly very different from where I come from, Sri Lanka. My advice is to always stay one step ahead in your interactions with financial institutions. Knowing what to expect will help you prepare better and allow you to negotiate more effectively when opportunities arise. Thankfully, the internet is full of helpful stories and experiences from other internationals that can guide you along the way.

Good luck on your journey towards having your dream home and financial prosperity in Denmark.

Alt det bedste!